Maximize Your Social Security in 2026: A 5-Step Guide

Anúncios

Understanding and strategically applying claiming age, earnings records, and spousal benefits are crucial steps to significantly increase your monthly Social Security payouts and secure your financial future in 2026.

Anúncios

Are you looking to make the most of your retirement income? Learning how to navigate the complexities of Social Security is paramount for a comfortable future. This guide will walk you through Maximizing Your Social Security in 2026: A 5-Step Guide to Increased Payouts, ensuring you’re well-equipped to make informed decisions.

Understanding Social Security Basics for 2026

Before diving into strategies, it’s essential to grasp the fundamental concepts of Social Security as they apply to 2026. This foundational knowledge will empower you to make more informed choices about your benefits. Social Security is a complex system, but understanding its core components is the first step toward optimizing your payouts.

Anúncios

The program is primarily funded through payroll taxes, known as FICA taxes. These contributions from your earnings throughout your working life determine your eligibility and the amount of your future benefits. The Social Security Administration (SSA) calculates your benefit amount based on your highest 35 years of earnings, adjusted for inflation.

Key Terms to Know

Familiarizing yourself with specific terminology is crucial. These terms will frequently appear in any discussion about Social Security and are vital for comprehending how your benefits are calculated and distributed.

- Full Retirement Age (FRA): This is the age at which you are entitled to receive 100% of your primary insurance amount (PIA). For those born in 1960 or later, FRA is 67.

- Primary Insurance Amount (PIA): The benefit you would receive if you start collecting at your full retirement age. All other benefit amounts are based on your PIA.

- Cost-of-Living Adjustment (COLA): An annual increase in Social Security benefits to offset inflation. The COLA for 2026 will be announced later, but it’s a critical factor in maintaining purchasing power.

Understanding these basic elements provides a solid framework. Your benefit amount isn’t arbitrary; it’s a direct reflection of your earnings history and the age at which you choose to claim. Being aware of these factors allows you to begin thinking strategically about your claiming decision and how it impacts your financial future.

Step 1: Verify Your Earnings Record Annually

Your Social Security benefit is directly tied to your lifetime earnings. Ensuring your earnings record is accurate is arguably the most critical first step in maximizing your future payouts. Errors in your record, even minor ones, can lead to a significant reduction in your benefits over time.

The Social Security Administration (SSA) maintains a record of your reported earnings throughout your career. It’s not uncommon for mistakes to occur, such as incorrect reporting by an employer, transposed numbers, or even missing years of earnings. These inaccuracies can compound over decades, resulting in a lower primary insurance amount (PIA) than you are rightfully owed.

How to Check Your Earnings Record

The process for reviewing your earnings record is straightforward and should be done regularly, ideally once a year. The SSA provides convenient online tools to facilitate this.

- Create an SSA Account: If you haven’t already, establish an account on the official Social Security Administration website (ssa.gov). This account provides secure access to your personal earnings statement.

- Review Your Statement: Once logged in, carefully examine your Social Security Statement. Pay close attention to your reported earnings for each year. Compare these figures against your W-2 forms or tax returns.

- Report Discrepancies Promptly: If you find any errors, contact the SSA immediately. You’ll need documentation, such as W-2s, pay stubs, or tax returns, to support your claim. The sooner you address discrepancies, the easier they are to resolve.

Proactive verification of your earnings record is a simple yet powerful way to protect your future Social Security benefits. Think of it as auditing your financial future; catching errors now can prevent substantial losses later. This annual check ensures that the foundation of your benefit calculation is as robust and accurate as possible.

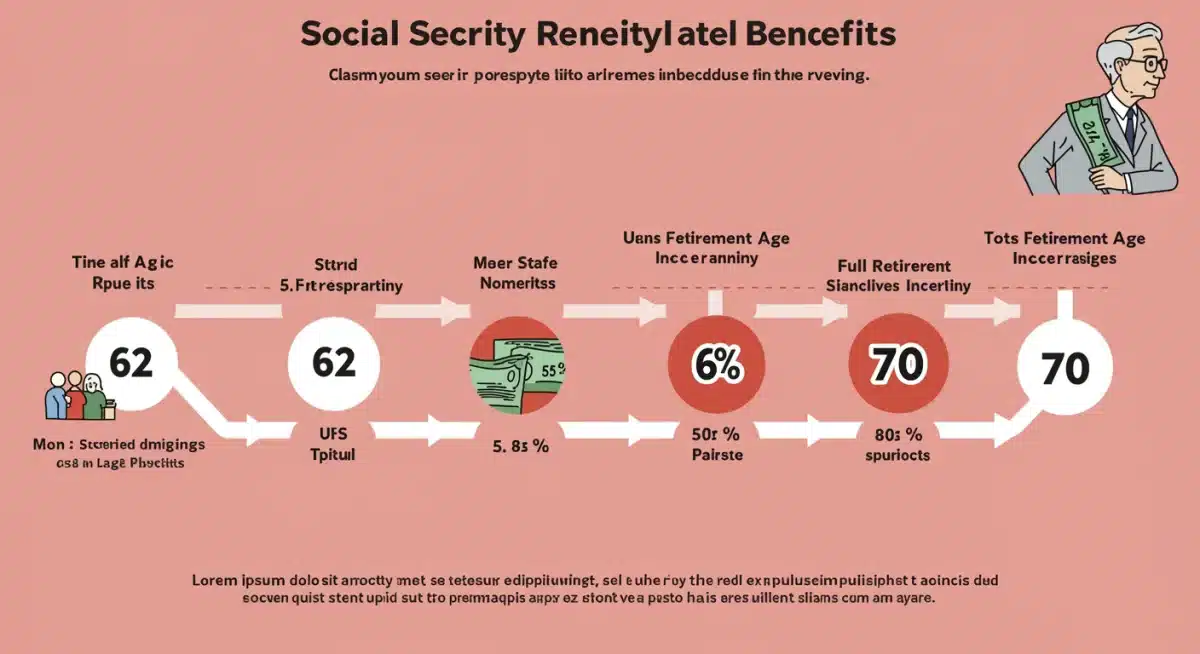

Step 2: Strategically Choose Your Claiming Age

The age at which you decide to claim your Social Security benefits has a profound impact on your monthly payout. This decision is one of the most significant financial choices you’ll make regarding your retirement income. While you can start receiving benefits as early as age 62, doing so comes with a permanent reduction.

Conversely, delaying your claim past your full retirement age (FRA) can significantly increase your monthly benefit. For each year you delay claiming beyond your FRA, up until age 70, you earn delayed retirement credits. These credits result in an 8% increase per year, making a substantial difference in your lifetime benefits.

Understanding the Trade-offs

There’s no one-size-fits-all answer to the ideal claiming age. Your personal circumstances, health, financial needs, and life expectancy all play a role in this complex decision.

- Claiming Early (Age 62): Results in a permanent reduction of up to 30% of your full benefit. While it provides income sooner, it means less money each month for the rest of your life.

- Claiming at Full Retirement Age (FRA): You receive 100% of your primary insurance amount. This is often a balanced approach for many retirees, offering a good monthly benefit without significant reductions or lengthy delays.

- Claiming Late (Up to Age 70): Each year you delay past FRA increases your benefit by 8% annually, up to age 70. This can result in a 24-32% higher monthly payout compared to your FRA benefit.

Consider your health and family longevity when making this choice. If you anticipate a long lifespan, delaying benefits might yield a higher total payout over your retirement. However, if health concerns suggest a shorter life expectancy, claiming earlier might be more advantageous. It’s a careful balance between immediate needs and long-term financial security.

Step 3: Maximize Your Earnings Before Claiming

Since your Social Security benefits are calculated based on your 35 highest-earning years, continuing to work and increase your income in the years leading up to retirement can have a substantial positive impact on your future payouts. Even if you’ve already accumulated 35 years of earnings, higher income in later years can replace lower-earning years in your past.

This strategy is particularly effective if you had periods of lower earnings, unemployment, or worked part-time earlier in your career. Replacing those lower-earning years with higher current income can significantly boost your average indexed monthly earnings (AIME), which is the basis for your primary insurance amount (PIA).

Strategies for Boosting Earnings

There are several practical ways to enhance your earnings during your peak years, directly influencing your Social Security benefit calculation. These strategies require planning but offer tangible rewards.

- Work Longer: If possible, consider extending your working career by a few years. Each additional year of higher earnings can replace a year of lower or zero earnings in your calculation.

- Increase Your Income: Explore opportunities for raises, promotions, or taking on additional responsibilities at your current job. Even a side hustle or part-time work can contribute to your overall earnings record.

- Avoid Zero-Earnings Years: If you’re nearing retirement, try to avoid years with no earnings, as these will be factored into your 35-year average as zero, pulling down your overall benefit.

Focusing on maximizing your earnings, especially in your prime earning years, is a proactive approach to increasing your Social Security benefits. It’s a direct way to contribute more to the system and, in turn, receive more back in retirement. This step complements the claiming age decision by building a stronger foundation for your benefit amount.

Step 4: Understand and Utilize Spousal Benefits

Social Security doesn’t just offer benefits to individual workers; it also provides spousal benefits, which can be a game-changer for married couples, divorced individuals, and even surviving spouses. Understanding these provisions is crucial for maximizing your household’s total Social Security income.

A spouse can claim up to 50% of their partner’s primary insurance amount (PIA) if that amount is higher than their own benefit based on their work record. This is especially beneficial if one spouse has significantly higher earnings or if one spouse did not work enough to qualify for their own benefits.

Key Considerations for Spousal Benefits

Navigating spousal benefits requires careful planning and an understanding of eligibility rules. These rules can be complex, so it’s wise to consult with the SSA or a financial advisor.

- Eligibility: To claim spousal benefits, you must generally be at least 62 years old, and your spouse must have already filed for their own benefits.

- Impact on Your Own Benefit: If you are eligible for both your own worker benefit and a spousal benefit, the SSA will pay you the higher of the two amounts. You cannot receive both in full.

- Divorced Spouses: You may be able to claim benefits on an ex-spouse’s record if the marriage lasted at least 10 years, you are currently unmarried, and you are at least 62. Your ex-spouse does not need to have filed for their benefits for you to claim, provided you’ve been divorced for at least two years.

- Surviving Spouses: Widows and widowers can often claim 100% of their deceased spouse’s benefit. This is a critical provision for financial security after the loss of a partner.

Coordinating claiming strategies between spouses can lead to a significantly higher total household benefit. For example, the higher-earning spouse might delay claiming until age 70 to maximize their individual benefit, while the lower-earning spouse might claim spousal benefits earlier. This intricate dance requires careful consideration of each partner’s earnings history, age, and health.

Step 5: Consider Your Tax Implications and Other Income

While the focus is often on increasing the gross amount of your Social Security benefits, it’s equally important to consider the net amount you’ll receive after taxes. For many retirees, a portion of their Social Security benefits can be subject to federal income tax, and in some states, state income tax as well.

The amount of your benefits subject to tax depends on your ‘provisional income,’ which includes your adjusted gross income (AGI), tax-exempt interest, and half of your Social Security benefits. Understanding these thresholds is vital for effective tax planning in retirement.

Navigating Taxable Benefits

Being aware of how your Social Security income interacts with other retirement income sources can help you plan for a more tax-efficient retirement. Proactive planning can minimize your tax burden.

- Federal Income Tax: Up to 50% of your benefits may be taxable if your provisional income is between $25,000 and $34,000 for an individual, or $32,000 and $44,000 for a married couple filing jointly. Up to 85% of your benefits may be taxable if your provisional income exceeds these upper thresholds.

- State Income Tax: Some states tax Social Security benefits. It’s crucial to understand the tax laws in your state of residence, as this can further impact your net benefits.

- Other Retirement Income: Income from pensions, 401(k)s, IRAs, and investments all contribute to your provisional income, potentially pushing your Social Security benefits into taxable territory.

Beyond taxes, evaluate how your Social Security benefits fit into your overall retirement income strategy. Will it cover your essential living expenses, or will it supplement other savings? Consider how healthcare costs, inflation, and unexpected expenses might impact your financial picture. A holistic view of your retirement income, including Social Security, taxes, and other assets, ensures a more secure and comfortable future.

Future Outlook and Planning for 2026 and Beyond

As we look towards 2026 and the years that follow, the landscape of Social Security is subject to ongoing discussion and potential adjustments. While the core principles remain, it’s wise to stay informed about any legislative changes that could impact future benefits. These changes might include modifications to the full retirement age, adjustments to the COLA formula, or alterations in taxation rules.

It is important to remember that Social Security is designed to be a foundation of retirement income, not necessarily the sole source. Therefore, integrating your Social Security strategy with other retirement savings vehicles, such as 401(k)s, IRAs, and personal investments, is crucial for comprehensive financial security.

Staying Informed and Adapting

The best financial plans are flexible and adaptable. Regularly reviewing your retirement strategy and staying updated on Social Security news will allow you to make necessary adjustments.

- Monitor SSA Announcements: Keep an eye on official Social Security Administration announcements regarding COLA, earnings limits, and any proposed legislative changes.

- Consult Financial Professionals: A qualified financial advisor specializing in retirement planning can provide personalized guidance, helping you navigate complex decisions and optimize your overall financial picture.

- Review Your Plan Annually: Life circumstances change, and so do financial markets. An annual review of your retirement plan, including your Social Security strategy, ensures it remains aligned with your goals.

By staying proactive and informed, you can ensure that your strategy for maximizing Social Security in 2026 remains robust and effective. The goal is not just to get the highest possible monthly payment, but to integrate that payment into a sustainable and resilient retirement plan that provides peace of mind for years to come. Your financial future is a journey, not a destination, and continuous adaptation is key.

| Key Point | Brief Description |

|---|---|

| Verify Earnings | Annually check your SSA record for accuracy to ensure correct benefit calculation. |

| Claiming Age | Delaying past Full Retirement Age (FRA) up to age 70 increases monthly payouts. |

| Maximize Earnings | Higher earnings in your top 35 years can significantly boost your benefit amount. |

| Spousal Benefits | Utilize spousal or survivor benefits for higher household income, if eligible. |

Frequently Asked Questions About Social Security in 2026

For individuals born in 1960 or later, including those planning for 2026, the Full Retirement Age (FRA) for Social Security benefits remains 67. Claiming benefits before this age will result in a permanent reduction, while delaying past it can increase your monthly payout.

Delaying your claim past your Full Retirement Age (FRA) up to age 70 can increase your monthly benefit by 8% per year through delayed retirement credits. This can lead to a substantially higher monthly payment for the rest of your life, significantly boosting your total lifetime benefits.

Yes, a portion of your Social Security benefits may be subject to federal income tax in 2026, depending on your provisional income. Some states also tax Social Security benefits. Understanding your income thresholds is crucial for proper tax planning in retirement.

Yes, you can work and receive Social Security benefits simultaneously. However, if you are below your Full Retirement Age, there are annual earnings limits. If you earn above these limits, a portion of your benefits will be withheld until you reach your FRA. These withheld benefits are not lost; they lead to a higher future monthly amount.

Your Social Security benefit calculation relies on your highest 35 years of indexed earnings. Verifying your earnings record annually with the SSA ensures that all your contributions are correctly recorded. Correcting any errors can prevent a lower benefit payout, ensuring you receive all the benefits you are entitled to based on your work history.

Conclusion

Successfully navigating the path to a secure retirement heavily relies on a well-thought-out Social Security strategy. By diligently applying these five steps—verifying your earnings, strategically choosing your claiming age, maximizing your income, understanding spousal benefits, and considering tax implications—you are well-positioned for Maximizing Your Social Security in 2026: A 5-Step Guide to Increased Payouts. Proactive planning and staying informed about potential changes will ensure your Social Security benefits provide the strongest possible foundation for your financial future.