Medicare Part B 2026: Understanding Premium Adjustments and What a 5.5% Increase Means for You

Anúncios

Understanding Medicare Part B Premium Adjustments for 2026: What a 5.5% Increase Means for You

Anúncios

As we look ahead, one topic that consistently captures the attention of millions of Americans, particularly those aged 65 and older, is the annual adjustment of Medicare premiums. Specifically, the projected 5.5% increase in Medicare Part B 2026 premiums is a significant development that warrants a deep dive. For many, Medicare Part B is a crucial component of their healthcare coverage, encompassing doctor visits, outpatient services, preventive care, and certain medical supplies. Understanding these adjustments is not just about knowing a number; it’s about comprehending the broader implications for personal finances, healthcare access, and future planning.

The Centers for Medicare & Medicaid Services (CMS) regularly evaluates and adjusts premiums to ensure the solvency and sustainability of the Medicare program. These adjustments are influenced by a complex array of factors, including healthcare utilization trends, pharmaceutical costs, technological advancements in medicine, and the overall economic landscape. A 5.5% increase for Medicare Part B 2026, while not definitive until official announcements, signals a notable rise that could impact the budgets of countless beneficiaries. This article aims to demystify these adjustments, explore the underlying reasons for such an increase, analyze its potential impact on your wallet, and provide actionable strategies to navigate these changes effectively.

The Mechanics of Medicare Part B Premiums

Before delving into the specifics of the 2026 projected increase, it’s essential to grasp how Medicare Part B 2026 premiums are determined. Unlike Medicare Part A, which is typically premium-free for most individuals who have paid Medicare taxes for a sufficient period, Part B requires a monthly premium. This premium is deducted directly from Social Security benefits for most recipients. The standard Part B premium is set annually, but some beneficiaries pay more due to the Income-Related Monthly Adjustment Amount (IRMAA).

Anúncios

Standard vs. IRMAA Premiums

The standard Medicare Part B 2026 premium applies to the majority of beneficiaries. However, if your modified adjusted gross income (MAGI) exceeds certain thresholds, you will pay IRMAA, which is an additional amount added to your standard premium. These income thresholds are also adjusted annually, meaning that even if your income remains stable, you could potentially move into a higher IRMAA bracket if the thresholds do not keep pace with inflation or if your income increases significantly. This tiered system ensures that those with higher incomes contribute more to the Medicare program, a principle designed to maintain fairness and financial stability.

Factors Influencing Premium Adjustments

Several critical factors contribute to the annual adjustments in Medicare Part B 2026 premiums. These include:

- Healthcare Spending Trends: The overall cost of healthcare services, including hospital outpatient care, physician services, and durable medical equipment, plays a significant role. If these costs rise, so too do the pressures on Part B premiums.

- Drug Costs: The price of prescription drugs, particularly high-cost specialty medications, is a major driver of Medicare expenditure. While Part D covers most prescription drugs, some medications administered in a doctor’s office or outpatient setting fall under Part B, directly influencing its costs.

- Utilization of Services: Changes in how often beneficiaries use Part B services can also impact premiums. An increase in the frequency of doctor visits, diagnostic tests, or outpatient procedures can lead to higher overall program costs.

- Medical Technology and Innovation: Advancements in medical technology, while beneficial for patient care, often come with a higher price tag. New diagnostic tools, treatment modalities, and medical devices can increase the cost of services covered by Part B.

- Legislation and Policy Changes: Congressional actions and policy decisions by CMS can directly affect premium calculations. These might include changes to benefit structures, provider payment rates, or cost-sharing requirements.

- Economic Conditions: Inflation, wage growth, and the overall health of the economy can indirectly influence healthcare costs and, subsequently, Medicare premiums.

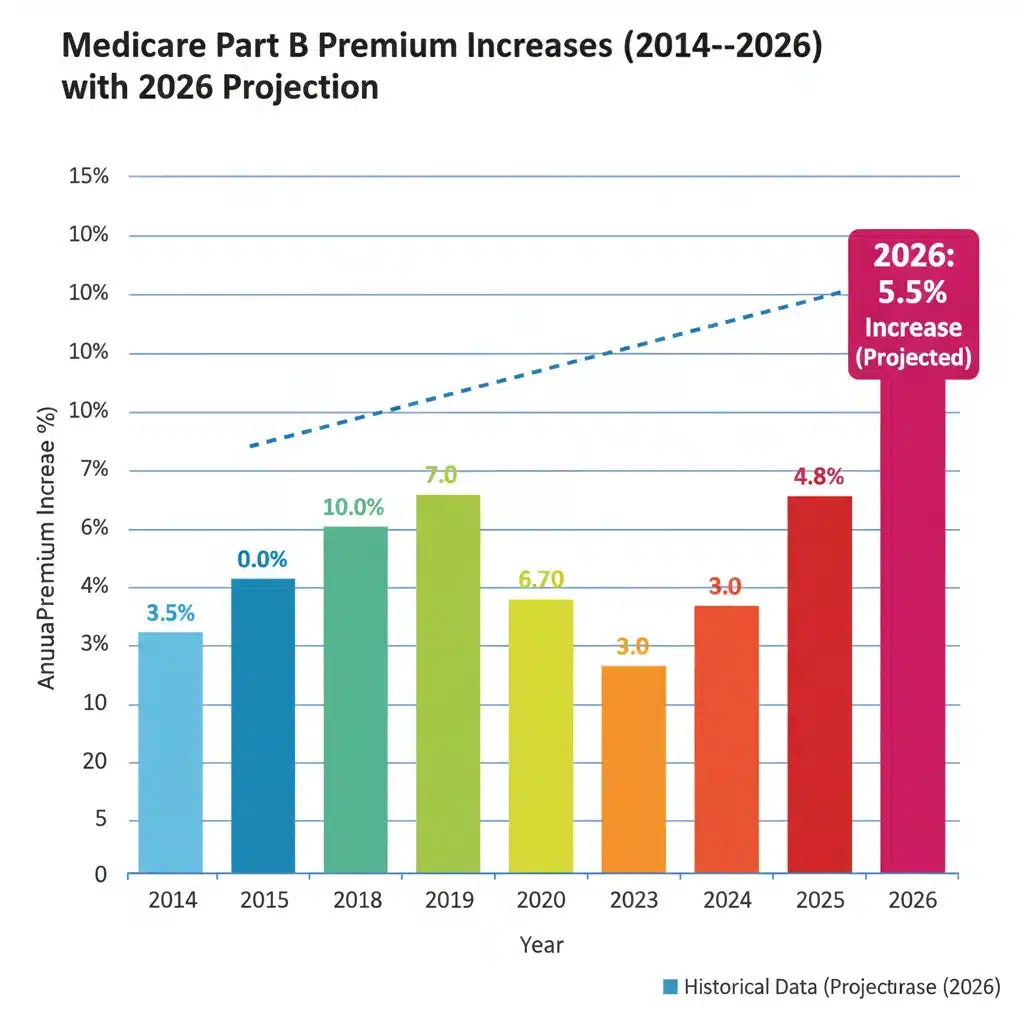

The Projected 5.5% Increase for Medicare Part B 2026: What’s Driving It?

A projected 5.5% increase in Medicare Part B 2026 premiums is a notable figure that signals ongoing challenges in managing healthcare costs. While the exact reasons for this specific projection will be detailed by CMS closer to the official announcement, several general trends likely contribute to such an outlook.

Rising Healthcare Utilization and Costs

The aging population in the United States means an increasing number of individuals are entering the Medicare system. As people age, their healthcare needs often become more complex and frequent, leading to higher utilization of services. Moreover, the cost of providing these services continues to climb due to various factors, including:

- Inflationary Pressures: The general increase in the cost of goods and services affects healthcare providers, leading to higher operating costs that are often passed on.

- Labor Shortages and Wage Growth: The healthcare sector, like many others, faces labor shortages, particularly for skilled professionals. This can drive up wages, which are a significant component of healthcare costs.

- Advancements in Medical Care: While life-saving, new treatments and technologies are frequently more expensive.

Impact of New Treatments and Technologies

The development of innovative medical treatments, especially in areas like oncology, rare diseases, and chronic condition management, often comes with a high price tag. Many of these treatments are administered in outpatient settings or by physicians, falling under Medicare Part B 2026 coverage. As more of these advanced therapies become available and widely adopted, they contribute to the overall expenditure of the Part B program, necessitating premium adjustments.

The ‘Hold Harmless’ Provision and Its Role

An important consideration in premium adjustments is the ‘Hold Harmless’ provision. This provision prevents an individual’s net Social Security benefit from decreasing due to an increase in their Medicare Part B premium. It applies to approximately two-thirds of Medicare beneficiaries who have their Part B premiums deducted directly from their Social Security checks. If the annual Social Security cost-of-living adjustment (COLA) is not sufficient to cover the Part B premium increase, the premium for these individuals is capped so that their net Social Security payment does not fall below the previous year’s level.

However, this provision does not apply to all beneficiaries. It does not protect:

- New Medicare enrollees.

- High-income beneficiaries who pay IRMAA.

- Beneficiaries who do not have their Part B premiums deducted from Social Security benefits.

- Beneficiaries whose income falls below a certain threshold and are eligible for state-funded Medicare Savings Programs.

For those not protected by ‘Hold Harmless,’ the full impact of the 5.5% increase in Medicare Part B 2026 will be felt directly.

Who Will Be Most Affected by the 5.5% Increase?

While a 5.5% increase in Medicare Part B 2026 premiums will affect all beneficiaries to some degree, certain groups will feel the impact more acutely.

High-Income Earners (IRMAA Beneficiaries)

Individuals subject to IRMAA will face a double whammy. Not only will their standard premium increase by 5.5%, but their additional IRMAA surcharge will also be recalculated based on their income. This means their total Part B premium could see a substantially larger dollar increase compared to those paying the standard premium, making financial planning even more critical for this group.

New Medicare Enrollees in 2026

Those enrolling in Medicare Part B for the first time in 2026 will immediately face the new, higher premium. Unlike existing beneficiaries who might be protected by the ‘Hold Harmless’ provision, new enrollees will pay the full standard premium from the outset, making their initial entry into Medicare more expensive than it would have been in previous years.

Beneficiaries Not Protected by ‘Hold Harmless’

As discussed, a significant portion of beneficiaries is not covered by the ‘Hold Harmless’ provision. This includes those who pay their premiums directly (not deducted from Social Security), those with higher incomes, and those who have recently enrolled. These individuals will experience the full brunt of the 5.5% increase in Medicare Part B 2026 premiums.

Strategies for Managing Rising Medicare Part B Costs

Facing a potential 5.5% increase in Medicare Part B 2026 premiums can be daunting, but several strategies can help beneficiaries manage these rising costs and ensure continued access to necessary healthcare.

1. Review Your Budget and Financial Plan

The first step is to thoroughly review your current budget and financial plan. Understand how the projected increase will impact your monthly expenses. If you’re on a fixed income, this exercise is particularly crucial. Look for areas where you might be able to adjust spending to accommodate the higher premium. Consider consulting with a financial advisor specializing in retirement planning to develop a robust strategy.

2. Explore Medicare Advantage (Part C) Plans

Medicare Advantage plans, offered by private insurance companies approved by Medicare, cover all the benefits of Original Medicare (Part A and Part B) and often include additional benefits like prescription drug coverage (Part D), vision, dental, and hearing. Many Medicare Advantage plans have $0 premiums beyond your Part B premium, and some even offer Part B premium give-back programs, which can effectively reduce your overall monthly cost. It’s essential to compare plans in your area, consider their network restrictions, out-of-pocket maximums, and overall coverage to see if a Medicare Advantage plan aligns with your healthcare needs and budget.

3. Investigate Medicare Supplement (Medigap) Plans

Medigap plans work differently than Medicare Advantage. They are designed to cover the ‘gaps’ in Original Medicare, such as deductibles, co-payments, and co-insurance. While Medigap plans come with their own separate premiums, they can significantly reduce your out-of-pocket costs for covered services. If you frequently use healthcare services, a Medigap plan, despite its additional premium, might save you money in the long run by covering the 20% co-insurance that Part B doesn’t pay. It’s crucial to compare different Medigap plans (A, B, C, D, F, G, K, L, M, N) to find one that best suits your needs and budget, especially considering the changes to plans C and F for new enrollees after January 1, 2020.

4. Check Eligibility for Medicare Savings Programs (MSPs)

Medicare Savings Programs (MSPs) are state-administered programs that help low-income beneficiaries pay for their Medicare premiums, deductibles, co-payments, and co-insurance. There are several types of MSPs, each with different income and resource limits. These programs can significantly alleviate the burden of rising Medicare Part B 2026 premiums. Even if you think your income is too high, it’s worth checking, as the eligibility criteria can be more generous than for other assistance programs. Contact your state’s Medicaid office or State Health Insurance Assistance Program (SHIP) for more information.

5. Review Your Prescription Drug Coverage (Part D)

While Part D covers most prescription drugs, ensuring you have the most cost-effective plan is vital. High drug costs can indirectly impact your overall healthcare budget, making it harder to absorb increases in Part B premiums. Annually, during the Open Enrollment Period, compare Part D plans to ensure your current plan still covers your medications at the best possible price. Small changes in your drug regimen or available plans can lead to significant savings.

6. Consider Preventive Care and Healthy Lifestyle Choices

Maintaining a healthy lifestyle through diet, exercise, and regular preventive care can help reduce the need for more extensive, costly medical interventions down the line. Medicare Part B covers a wide range of preventive services, often at no additional cost, including annual wellness visits, screenings for various conditions, and immunizations. Utilizing these services can help detect health issues early, potentially preventing more severe and expensive complications. Proactive health management is a powerful tool in controlling overall healthcare expenditures.

7. Stay Informed and Advocate

Knowledge is power. Stay informed about legislative discussions and proposed changes to Medicare. Organizations like AARP and the Medicare Rights Center provide valuable resources and advocate for beneficiaries. Understanding the political and economic landscape surrounding Medicare can help you anticipate future changes and make informed decisions about your healthcare coverage and financial planning. Consider reaching out to your elected officials to voice your concerns about rising healthcare costs and the impact of premium increases.

The Broader Implications of Rising Medicare Costs

The projected 5.5% increase in Medicare Part B 2026 premiums is not an isolated event; it’s part of a larger trend of increasing healthcare costs in the United States. This trend has significant implications beyond individual beneficiaries:

Impact on Seniors and Fixed Incomes

For many seniors living on fixed incomes, even a modest increase in premiums can create financial strain. It can force difficult choices between essential healthcare and other necessities like food, housing, or utilities. This highlights the ongoing need for robust social safety nets and affordable healthcare solutions.

Sustainability of the Medicare Program

The rising costs of healthcare, reflected in premium adjustments, also raise questions about the long-term financial sustainability of the Medicare program. Policymakers continuously grapple with balancing comprehensive coverage, affordability for beneficiaries, and the fiscal health of the trust funds. The projected increases underscore the urgency of finding sustainable solutions for healthcare funding.

Healthcare Policy Debates

Premium adjustments invariably fuel debates about healthcare policy. Discussions often center on drug pricing reform, provider payment models, administrative efficiency, and the role of private insurance in Medicare. The 5.5% increase for Medicare Part B 2026 will undoubtedly add another layer to these complex and critical conversations.

Preparing for the Future: What to Expect

While the 5.5% increase for Medicare Part B 2026 is currently a projection, it serves as an important warning sign. Official announcements regarding the exact premium amounts typically occur in the fall of the preceding year. This gives beneficiaries a few months to prepare and make necessary adjustments to their healthcare plans.

During the annual Medicare Open Enrollment Period (October 15 to December 7), beneficiaries have the opportunity to review and change their Medicare Advantage plans, Part D prescription drug plans, or switch from Original Medicare to a Medicare Advantage plan (or vice versa). This period is crucial for reacting to new premium announcements and ensuring your coverage remains optimal for your health needs and financial situation.

It is advisable to:

- Stay updated: Monitor official Medicare sources, such as Medicare.gov, and reputable news outlets for the confirmed 2026 premium amounts.

- Assess your needs: Re-evaluate your healthcare usage, prescription drug needs, and overall health status.

- Compare plans: Use the Medicare Plan Finder tool on Medicare.gov to compare all available options in your area, including Medicare Advantage and Part D plans.

- Seek personalized advice: Consult with a licensed insurance agent specializing in Medicare or a SHIP counselor for personalized guidance. They can help you understand your options and make informed decisions based on your unique circumstances.

Conclusion: Navigating the Evolving Landscape of Medicare

The projected 5.5% increase in Medicare Part B 2026 premiums underscores the dynamic and often challenging nature of healthcare costs. While these adjustments can be concerning, they are a fundamental part of maintaining the Medicare program’s ability to provide essential health services to millions of Americans. By understanding the factors driving these changes, identifying how they might specifically impact you, and proactively exploring available strategies, you can effectively manage your healthcare expenses and ensure you continue to receive the care you need.

Staying informed, reviewing your options during Open Enrollment, and seeking expert advice are key steps in navigating the evolving landscape of Medicare. The goal is not just to absorb the increase but to strategically adapt your coverage and financial planning to minimize its impact, ensuring your health and financial well-being remain secure in the years to come.