2026 Mortgage Rate Trends: Secure 6.1% Fixed Before Increases

Anúncios

The Latest 2026 Mortgage Rate Trends: Securing a Fixed 6.1% Before Projected Increases

Anúncios

As we navigate the ever-evolving financial landscape, understanding future housing market dynamics is crucial for both prospective homebuyers and current homeowners. The year 2026 is rapidly approaching, and with it comes a renewed focus on 2026 mortgage rates. Experts are increasingly forecasting a period of rising interest rates, with a significant emphasis on the potential for fixed rates to climb beyond the current attractive threshold, possibly surpassing 6.1%. This comprehensive guide will delve into the factors driving these predictions, provide actionable insights, and help you strategize to secure the best possible mortgage terms before these anticipated increases take hold. The decision to buy a home or refinance an existing mortgage is one of the most significant financial commitments you’ll ever make. Therefore, being well-informed about the trajectory of 2026 mortgage rates is not just advantageous; it’s essential for making financially sound choices.

The housing market is a complex ecosystem, influenced by a myriad of global and domestic economic forces. From inflation and central bank policies to employment figures and geopolitical events, each element plays a pivotal role in shaping the cost of borrowing. For those considering a home purchase or a refinance in the next few years, the outlook for 2026 mortgage rates presents both challenges and opportunities. While the prospect of higher rates can be daunting, early preparation and strategic planning can mitigate potential risks and even turn them into advantages. This article aims to equip you with the knowledge to navigate these waters effectively, ensuring you are well-prepared for what lies ahead in the realm of mortgage financing. We will explore the macroeconomic environment, the Federal Reserve’s likely actions, and the direct implications for your mortgage payments, all while keeping the critical benchmark of 6.1% fixed rates in perspective.

Understanding the Current Mortgage Rate Landscape

Before we project into 2026, it’s vital to understand the current state of mortgage rates. Recent years have seen unprecedented volatility, with rates fluctuating significantly due to various economic shocks and policy responses. The pandemic, supply chain disruptions, and geopolitical tensions have all contributed to an environment where predicting interest rate movements has become more challenging than ever. Currently, fixed mortgage rates have settled into a range that, while higher than the historic lows of a few years ago, is still considered favorable by many. However, this stability is perceived by many analysts as a temporary reprieve before potential upward adjustments. The average 30-year fixed-rate mortgage has hovered around the 6% mark, making the 6.1% forecast for 2026 mortgage rates a critical benchmark. This current environment is a direct result of the Federal Reserve’s efforts to combat inflation, which has seen a series of aggressive interest rate hikes. These hikes directly influence the prime rate, which in turn impacts lending rates across the board, including mortgages.

Anúncios

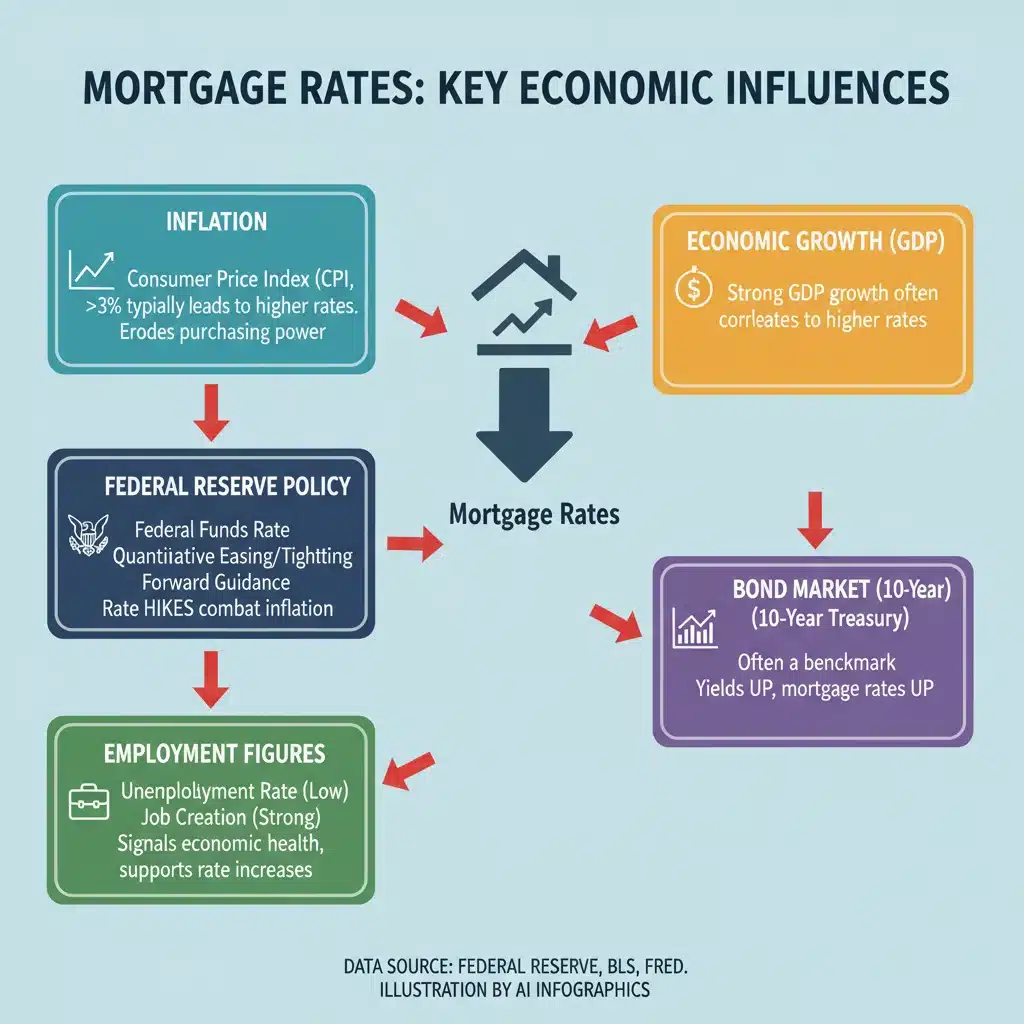

The interplay between inflation, the Federal Reserve’s monetary policy, and bond yields is fundamental to understanding mortgage rate movements. Mortgage rates are not directly set by the Fed; rather, they are closely tied to the yield on the 10-year Treasury bond. When inflation is high, investors demand higher returns on bonds, leading to increased yields, which in turn push mortgage rates up. The Fed’s role is to manage inflation, primarily through adjusting the federal funds rate. When the Fed raises this rate, it makes borrowing more expensive for banks, and this cost is then passed on to consumers in the form of higher loan rates. Therefore, any anticipation of continued inflation or further tightening by the Fed directly impacts the outlook for 2026 mortgage rates. Keeping a close eye on these economic indicators is paramount for anyone looking to enter the housing market or refinance their existing mortgage. The current landscape, while seemingly stable, is underpinned by a delicate balance of these powerful economic forces, making foresight and planning exceptionally important.

Key Economic Indicators Shaping 2026 Mortgage Rates

Several critical economic indicators will dictate the direction of 2026 mortgage rates. Understanding these factors can help you make more informed decisions about your mortgage strategy. The primary drivers include inflation, Federal Reserve policy, employment data, and global economic stability.

Inflationary Pressures

Inflation remains a dominant factor. Persistent inflation erodes the purchasing power of money, leading investors to demand higher yields on their investments, including mortgage-backed securities. If inflation remains stubbornly high or experiences a resurgence, the Federal Reserve will likely continue its hawkish stance, leading to higher interest rates. The current inflation rate, while showing signs of moderating from its peak, is still above the Fed’s long-term target of 2%. Any indications that inflation is not retreating as quickly as hoped could trigger further rate hikes, impacting 2026 mortgage rates significantly. Monitoring the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index will provide crucial insights into the future trajectory of inflation and, consequently, mortgage rates.

Federal Reserve Monetary Policy

The Federal Reserve’s actions are perhaps the most direct influence on mortgage rates. Through its open market operations and adjustments to the federal funds rate, the Fed aims to control the money supply and manage inflation. The market widely anticipates that the Fed will continue to monitor economic data closely. If economic growth remains robust and inflation proves sticky, the Fed may opt for additional rate increases or maintain higher rates for a longer period than currently expected. This ‘higher for longer’ scenario would undoubtedly push 2026 mortgage rates upwards, potentially well beyond the 6.1% mark. Conversely, a significant economic downturn or a rapid decline in inflation could prompt the Fed to cut rates, offering some relief to borrowers. However, the current consensus leans towards a more conservative approach from the Fed, prioritizing inflation control over stimulating growth through lower rates.

Employment Data and Economic Growth

A strong labor market and robust economic growth often lead to higher inflation and, subsequently, higher interest rates. When employment is high and wages are rising, consumer spending tends to increase, fueling inflationary pressures. The unemployment rate, job creation numbers, and wage growth figures are all closely watched by the Fed and market analysts. A cooling labor market, on the other hand, could signal a slowdown in economic activity, potentially leading the Fed to ease its monetary policy. For 2026 mortgage rates, a sustained period of low unemployment and strong wage growth would likely contribute to higher rates, as the economy would be perceived as strong enough to withstand tighter monetary conditions. Conversely, a weakening job market might provide a downward pull on future mortgage rates, though this would come at the cost of broader economic concerns.

Global Economic Stability and Geopolitical Events

The global economic environment and geopolitical events also play a role, albeit often indirectly. International conflicts, trade disputes, or economic crises in major global economies can create uncertainty, leading investors to seek safe-haven assets like U.S. Treasury bonds. This increased demand can temporarily push bond yields down, which might offer some downward pressure on mortgage rates. However, these events can also disrupt supply chains and fuel inflation, counteracting any potential rate relief. The interconnectedness of the global economy means that events far from home can still have a tangible impact on 2026 mortgage rates. For example, energy price shocks due to geopolitical tensions can significantly contribute to inflation, forcing central banks to react with tighter monetary policies.

Why 6.1% is a Critical Benchmark for 2026 Mortgage Rates

The figure of 6.1% for fixed 2026 mortgage rates is not an arbitrary number; it represents a significant threshold for several reasons. Historically, mortgage rates have fluctuated, and while a 6% rate might seem high compared to the sub-3% rates seen during the pandemic, it is still within a reasonable historical context. However, the concern isn’t just the absolute number but the direction of travel. Many financial models and expert forecasts suggest that once rates breach a certain psychological or resistance level, they tend to accelerate their upward trajectory. For many, 6.1% is seen as that critical point where the market could gain momentum in pushing rates higher, making homeownership less affordable for a broader segment of the population.

From an affordability perspective, crossing the 6.1% threshold means a tangible increase in monthly mortgage payments. For a typical home loan, even a half-percentage point increase can translate into hundreds of dollars more per month, significantly impacting a household’s budget. This directly affects purchasing power and can cool down demand in the housing market. Moreover, for those looking to refinance, securing a rate below 6.1% now could lock in substantial savings over the life of the loan, especially if rates continue to climb. The psychological impact of rising rates also plays a role; as rates increase, potential buyers may become more hesitant, leading to a slowdown in market activity. Therefore, understanding 6.1% as a critical benchmark helps to frame the urgency and importance of making informed decisions about your mortgage strategy well in advance of 2026.

Strategies to Secure Favorable Mortgage Rates Before 2026

Given the projections for rising 2026 mortgage rates, proactive planning is essential. Here are several strategies to consider to secure a favorable rate and minimize the impact of future increases:

1. Act Sooner Rather Than Later

If you are contemplating buying a home or refinancing, delaying your decision might prove costly. The general consensus among experts is that rates are more likely to rise than fall significantly in the lead-up to 2026. Locking in a rate now, especially if you can get one below or around the 6.1% mark, could save you a substantial amount over the life of your loan. This doesn’t mean rushing into a decision, but rather accelerating your research, pre-approval process, and property search. The current market, while challenged by inventory, still offers opportunities for those who are prepared to act decisively.

2. Strengthen Your Financial Profile

Lenders offer the best rates to borrowers with strong financial profiles. Before applying for a mortgage, focus on improving your credit score, reducing your debt-to-income ratio, and increasing your down payment savings. A higher credit score signals lower risk to lenders, often qualifying you for lower interest rates. A lower debt-to-income ratio demonstrates your ability to manage monthly payments, while a larger down payment reduces the loan amount, thereby lowering your monthly payments and potentially securing a better rate. These improvements can make a significant difference in the rate you are offered, potentially helping you stay below the 6.1% threshold for 2026 mortgage rates.

3. Explore Different Mortgage Products

While 30-year fixed-rate mortgages are popular, it’s worth exploring other options. Adjustable-Rate Mortgages (ARMs) often start with lower interest rates for an initial period (e.g., 5, 7, or 10 years) before adjusting. If you plan to sell your home or refinance before the adjustment period ends, an ARM might offer a lower initial payment. However, be aware of the risks associated with ARMs, as rates can increase significantly after the fixed period. Also, consider shorter-term fixed mortgages (e.g., 15 or 20 years), which typically come with lower interest rates but higher monthly payments. A mortgage broker can help you compare different products and determine which one best suits your financial goals and risk tolerance, especially in the context of anticipated 2026 mortgage rates.

4. Get Pre-Approved

Obtaining a mortgage pre-approval is a crucial step. It not only gives you a clear understanding of how much you can afford but also locks in an interest rate for a specific period (typically 30 to 90 days). This protects you from potential rate increases while you search for a home. If rates drop during your pre-approval period, you might even be able to renegotiate for a lower rate. Pre-approval also makes you a more attractive buyer to sellers, as it demonstrates your financial readiness. In a market where 2026 mortgage rates are expected to rise, having a pre-approved rate can provide significant peace of mind and financial security.

5. Consider a Rate Lock

When you find a property and are ready to finalize your mortgage, consider a rate lock. A rate lock guarantees your interest rate for a certain period, usually between 30 and 60 days, while your loan is being processed. This protects you from market fluctuations and ensures that you secure the rate you were quoted, even if general rates increase during that time. Some lenders offer ‘float-down’ options, which allow you to take advantage of a lower rate if market rates fall before your closing. Given the anticipated upward trend for 2026 mortgage rates, a rate lock is a prudent step to safeguard your financial planning.

Impact of Rising Rates on Homebuyers and Homeowners

The projected increase in 2026 mortgage rates, particularly if they surpass 6.1%, will have a multi-faceted impact on both prospective homebuyers and existing homeowners.

For Homebuyers:

- Reduced Affordability: Higher interest rates directly translate to higher monthly mortgage payments, reducing the amount of home a buyer can afford. This can push some buyers out of the market entirely or force them to compromise on their desired home features or location.

- Increased Competition for Lower Rates: As rates rise, there might be a rush among buyers to secure loans before further increases, potentially leading to increased competition for favorable terms.

- Shift in Market Dynamics: A slowdown in buyer demand due to higher rates could lead to a more balanced market, or even a buyer’s market in some areas, where sellers may need to adjust their expectations. However, this often comes at the cost of higher borrowing costs.

For Homeowners:

- Refinancing Challenges: Homeowners looking to refinance their existing mortgages to lower their payments or tap into their home equity will find it more challenging to secure a rate lower than their current one, especially if their original mortgage was obtained during a period of historically low rates.

- Impact on Home Equity Lines of Credit (HELOCs) and Adjustable-Rate Mortgages (ARMs): For those with HELOCs or ARMs, rising interest rates will directly increase their monthly payments, potentially straining household budgets.

- Property Value Appreciation: While not a direct impact of rates, a slowdown in the housing market due to higher rates could temper property value appreciation, affecting homeowners’ equity growth.

Long-Term Outlook and Expert Predictions for 2026 Mortgage Rates

The long-term outlook for 2026 mortgage rates is subject to ongoing debate among economists and financial analysts. While the immediate future points towards potential increases, the very long-term picture is less clear. Factors such as technological advancements, demographic shifts, and evolving global economic structures could influence rates beyond 2026.

Many experts predict that the era of ultra-low interest rates is unlikely to return in the foreseeable future. The global economy is recalibrating after years of unprecedented monetary stimulus, and central banks are signaling a more disciplined approach to inflation management. This suggests that while rates might fluctuate, they are more likely to settle at a higher equilibrium than what we’ve seen in the last decade. Some forecasts suggest that 2026 mortgage rates could stabilize in the mid-6% to low-7% range, assuming inflation is brought under control without triggering a severe recession. However, these are just predictions, and the actual trajectory will depend on a multitude of unpredictable events.

It’s important for individuals to develop a long-term financial strategy that accounts for various interest rate scenarios. This might involve building a stronger financial buffer, making extra mortgage payments when possible, or regularly reviewing and adjusting financial plans. Staying informed about economic news and expert analyses will be key to adapting to the evolving landscape of 2026 mortgage rates and beyond. The housing market is cyclical, and understanding these cycles, along with the underlying economic drivers, will empower you to make prudent decisions that safeguard your financial future.

Conclusion: Navigating the Future of 2026 Mortgage Rates

The prospect of rising 2026 mortgage rates, particularly the potential to exceed a fixed 6.1%, presents a significant consideration for anyone involved in the housing market. The confluence of persistent inflationary pressures, the Federal Reserve’s commitment to price stability, and other economic indicators all point towards a challenging borrowing environment in the coming years. However, knowledge and proactive planning can transform these challenges into opportunities.

By understanding the economic forces at play, strengthening your financial profile, exploring diverse mortgage products, and acting decisively to secure favorable terms, you can mitigate the impact of anticipated rate increases. Whether you are a first-time homebuyer, an experienced investor, or a homeowner considering refinancing, the time to prepare is now. Don’t wait for rates to climb further; take the necessary steps to lock in the best possible mortgage rate, ideally before the 6.1% mark becomes a historical artifact of a more affordable past.

Staying informed, consulting with financial advisors, and continuously evaluating your options will be crucial in navigating the evolving landscape of 2026 mortgage rates. The future of homeownership and mortgage financing is dynamic, but with careful planning and strategic execution, you can secure your financial future and achieve your housing goals, regardless of where interest rates ultimately settle.